Crypto was born without borders; taxes were not. As digital assets flow across exchanges, wallets, and protocols, they leave a paper trail that every jurisdiction now seeks to read in its own language. By 2025, the question is no longer whether crypto is taxable, but how-what counts as income, what counts as a gain, and who must report it, when, and to whom.

Around the world, lawmakers and tax authorities are moving from improvisation to playbook. Cross-border reporting frameworks are being phased in, domestic guidance is catching up to staking, NFTs, and DeFi, and enforcement is getting more coordinated. Yet beneath this convergence, national differences remain stark. A swap can be a taxable disposal in one country and a non-event in another. Airdrops may be ordinary income here and capital in nature there. Some systems exempt small personal-use payments; others apply VAT or GST to certain tokens. The labels-property, currency, commodity, security-still shape the bill.

This country-by-country guide maps that terrain. For each jurisdiction, it sets out how crypto is classified, what triggers taxation, the rates and holding periods that matter, how losses and costs are treated, and the treatment of mining, staking, DeFi, NFTs, stablecoins, and derivatives. It also notes reporting forms and deadlines, record-keeping expectations, withholding rules, penalties, and any announced changes on the horizon.

Think of it as an atlas rather than a verdict: a way to compare regimes, spot where your activities intersect with local rules, and prepare the questions you’ll take to a professional. The landscape is moving, but with a clear map and a consistent legend, 2025’s global crypto taxation becomes navigable-one country at a time.

Taxable events around the world: trading, swaps, staking, airdrops and NFTs

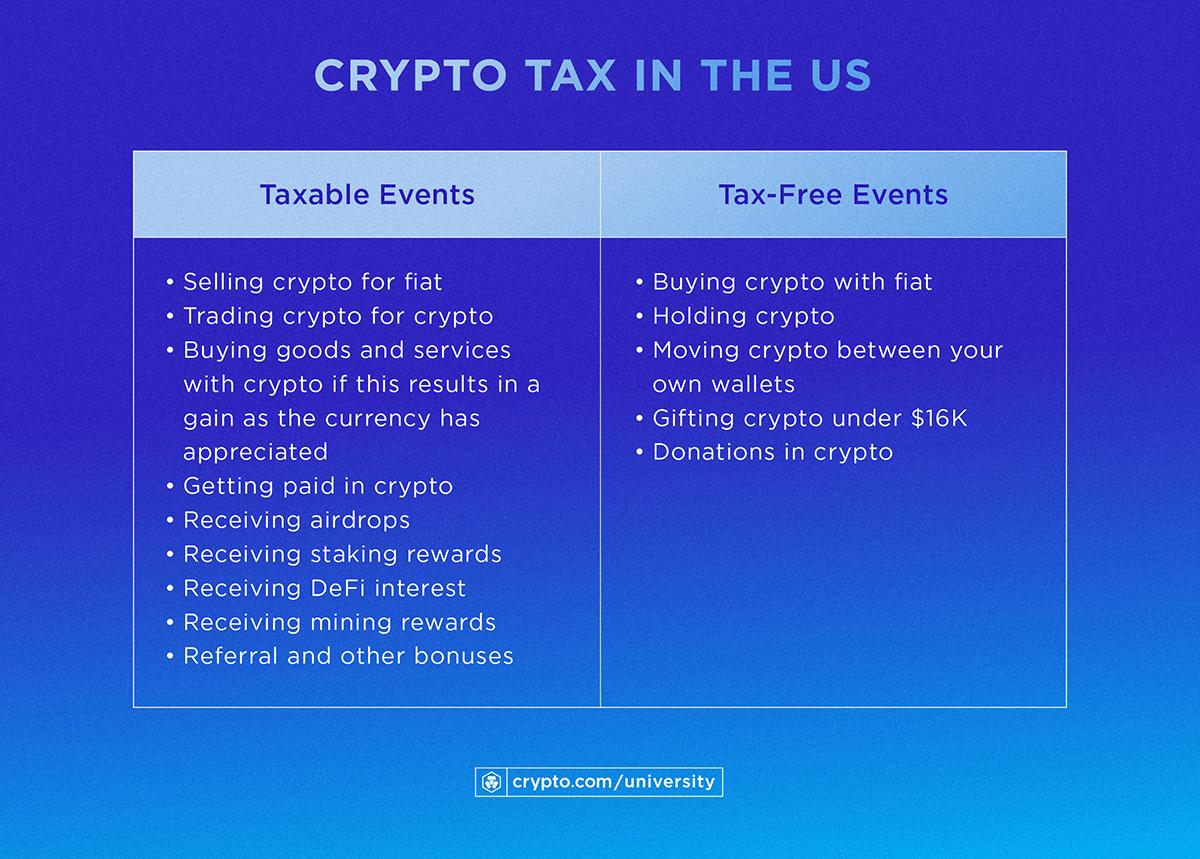

Across jurisdictions, the line between a harmless on-chain click and a taxable move is where “value is realized.” Most countries treat a sale for fiat as a clear disposal, but many also capture crypto‑to‑crypto conversions, DeFi liquidity moves, and NFT trades. The big swing factor is whether authorities see newly created or received tokens as income at fair market value on the day they hit your wallet, or only tax you later on capital gains when you sell. That single policy choice divides how staking flows, airdrops, and reward mechanics show up on your return.

- Trading: Selling for fiat, or spending crypto on goods/services, is widely taxed; rates vary by holding period and status.

- Swaps: Token‑to‑token exchanges are often treated like a sale plus purchase; a few places defer if no fiat is realized.

- Staking/Yield: Many tax rewards as income at receipt; others focus on gains when those rewards are later sold.

- Airdrops: Some tax on receipt if you have control; elsewhere, taxation generally waits until disposal unless tied to work.

- NFTs: Treated as digital assets in most regions; some apply collectible‑style rules or special rates in defined cases.

| Country | Trading/Swaps | Staking | Airdrops | NFTs |

|---|---|---|---|---|

| United States | Capital gains; swaps taxable | Income at receipt | Income at receipt (control) | Case‑by‑case; some collectible look‑through |

| United Kingdom | CGT on disposals incl. swaps | Often income; CGT on sale | Income if earned; CGT on disposal | CGT rules apply |

| Germany | Private sale rules; holding period matters | Income; holding may extend | Often income; CGT on sale | Taxed like other crypto |

| Australia | CGT event; swaps taxable | Ordinary income | Income at receipt | CGT asset |

| Japan | Taxable at progressive rates | Income at receipt | Income at receipt | Taxed similarly |

| India | 30% on gains; TDS on transfers | Taxable; specifics evolving | Generally taxable | Covered as VDA |

| Singapore | No CGT; business income possible | Taxed if revenue in nature | Taxed if revenue in nature | Generally capital; business rules may apply |

| Brazil | Gains taxable; swaps count | Income at receipt | Income on receipt/sale | CGT on disposal |

| UAE | Generally no personal tax | Business contexts taxable | Business contexts taxable | Generally no personal tax |

Record‑keeping is the quiet differentiator: accurate timestamps, local‑currency fair market values, and fee basis can change outcomes across borders. Deductibility of gas fees, wash‑sale rules, and the treatment of wrapping/bridging or DeFi liquidity tokens vary widely, so aligning your categorization with local guidance is essential-especially when the same click can be a mere reposition in one country and a full taxable disposal in another.

Country snapshots and effective rates: capital gains versus income, exemptions and holding period rules

What really bites your crypto returns isn’t just the headline rate-it’s how a country classifies the gain, whether there’s an exemption, and if a longer hold unlocks relief. Broadly, you’ll see regimes split between capital gains treatment (sometimes with long-term incentives) and ordinary-income treatment (where trading, staking, mining, or high-frequency activity can be taxed like a job). Watch for thresholds, de minimis rules, and how staking/DeFi rewards are characterized; these details often decide the effective rate you actually pay.

- Long-hold friendly: Germany, Portugal, Australia reward patience with 0% or discounts after 12 months.

- Income-first or flat regimes: India’s 30% and Japan’s progressive income model leave no long-term relief.

- Zero-tax hubs (for individuals): UAE and Singapore often exempt private gains but tax business activity.

- Allowances and thresholds: UK annual CGT allowance, Germany’s €600 de minimis, Italy and Brazil use small exemptions or tiers.

| Country | Primary Treatment | Effective Rates | Exemptions | Holding-Period Rule |

|---|---|---|---|---|

| United States | CG vs. Income | ST: ordinary; LT: 0%/15%/20% | None general | LT if held >1 year |

| Germany | Private sale (CG-like) | 0% >1y; else progressive | ~€600 de minimis | Tax-free after 1 year |

| Portugal | Capital gains | ~28% <1y; 0% >1y | None notable | Exempt after 365 days |

| India | Special VDA tax | 30% flat (+1% TDS) | No loss offsets | No LT/ST relief |

| Singapore | No CGT; business = income | 0% if investment; income 0-22% | None general | N/A (facts-and-circumstances) |

| United Kingdom | Capital gains | 10%/20% (band-based) | Annual CG allowance | No LT discount |

| Australia | CG vs. Income | Marginal; 50% CG discount >12m | None CG-specific | Discount after 12 months |

| Canada | CG vs. Business income | 50% inclusion at marginal rates | Loss netting allowed | No LT/ST distinction |

| UAE | Personal: often 0% CG | 0% personal; 9% corporate | Free-zone nuances | N/A for personal CG |

| Japan | Misc. income (most cases) | Progressive up to ~55% | Loss limits apply | No LT relief |

Effective rates hinge on behavior: a swing trader in the U.S. may face ordinary rates while a long-term saver slips into 0-20%; a Portuguese holder can go from ~28% to 0% after a year; a German investor’s €600 de minimis can erase small gains. In “no-CGT” places, regular trading or staking can still be taxed as income. Build your plan around three levers-classification (CG vs. income), reliefs (allowances, de minimis, offsets), and time (12 months is a common pivot)-and your real tax bite often looks very different from the headline number.

Reporting and enforcement architecture: exchange statements, wallet tracing, information sharing and deadlines

In 2025, tax oversight is shifting from detective work to data plumbing: standardized exchange reports flow into revenue systems, on-chain trails are stitched across bridges and mixers, and cross-border pipes are opening for near‑real‑time reconciliation. Expect exchange/broker statements (often cost‑basis aware) to pair with chain analytics that cluster self‑custody wallets to known identities, while Travel Rule metadata and sanctions flags enrich event timelines. Authorities coordinate through frameworks like CARF (pilot adoption), DAC8 (EU), legacy CRS/FATCA, and joint task forces such as the J5, tightening mismatches between what platforms report and what taxpayers file.

- Exchange statements: gross proceeds, adjusted basis, lot‑level disposals, staking/airdrop lines, plus unique IDs to reconcile with TXIDs.

- Wallet tracing: cluster heuristics, bridge hops, CEX<>DEX pivots, mixer exposure scores, NFT royalties and MEV tips attribution.

- Information sharing: CARF/CRS gateways, DAC8 intra‑EU flows, bilateral treaty requests, Travel Rule payloads between VASPs.

- Deadline cadence: pre‑fill windows in Q1-Q2, extension options in select markets, escalating penalties for late or non‑matched reports.

For filers, the practical response is a lean evidence stack and a calendar that respects both platform cutoffs and statutory due dates. Pull every CEX/broker annual statement, export full TX histories from DEXes and self‑custody, and tag complex events (wrapping, LP tokens, perpetuals funding, rebase, liquid staking). Keep oracle prices and FX at time of disposition, document cost‑basis methods, and archive chain‑analysis summaries for audits. Set reminders for statutory filings, extension triggers, and response windows to “soft letters.”

- Keep: wallet maps, TXIDs, price sources, gas logs, staking reward timestamps.

- Match: CEX reports to on‑chain sends/receipts; explain gaps (dust, failed TX, burn).

- Label: DeFi flows (borrow vs. dispose), NFT mints/resales, bridge‑in/bridge‑out neutrality.

- Calendar: typical filing windows below; verify local rules and extensions.

| Jurisdiction | Exchange statements | Wallet tracing | Info‑sharing | Typical deadline |

|---|---|---|---|---|

| United States | 1099‑DA/C emerging | High | Domestic + J5 | Mid‑Apr |

| European Union (DAC8) | Platform reports to tax | High | DAC8/CRS | Q2 (varies) |

| United Kingdom | HMRC‑aligned summaries | High | CRS + CARF‑ready | Jan 31 |

| Australia | ATO data‑matching | High | CRS + CARF‑ready | Oct 31 |

| India | VDA reports + TDS | Medium‑High | CRS | Jul 31 |

| Japan | Domestic exchange feeds | High | CRS | Mar 15 |

| Singapore | Platform statements (var.) | Medium | CRS | Mid‑Apr |

| Brazil | Monthly crypto reports | Medium‑High | CRS | Late May |

| UAE | VASPs under VARA | Medium | CRS | N/A (personal) |

Practical moves to lower liability legally: choose residency before realization, track basis across wallets, harvest losses, use entities with real substance

Timing is a tax tool. Align where you’re tax resident before gains crystallize-check treaty tie‑breakers, exit taxes, and 183‑day thresholds, and look for arrival step‑ups where available. Meanwhile, make basis bulletproof: pick a locally accepted method (FIFO, LIFO, or specific identification) and apply it consistently across CEX, DEX, L2s, and bridges. Include fees, wraps/unwraps, re-staking derivatives, and airdrop fair values; preserve TX hashes, chain IDs, and CSV/API exports to reconcile wallets into a single ledger that an auditor can follow line‑by‑line.

- Anchor status: secure a tax residency certificate; document deregistration from your prior country; map treaty tie‑breakers (home, vital interests, habitual abode).

- Pre‑move sequencing: complete disposals or rebases before crossing day‑count thresholds; avoid post‑move “look‑through” anti‑avoidance triggers.

- Lot discipline: use specific ID where accepted; tag lots at acquisition with screenshots and memos.

- Unified ledger: maintain an address map; monthly exports from each venue; reconcile bridges, LP adds/removes, and NFT trades.

- Evidence vault: retain statements, oracle prices, and fee records; store immutable proofs (TX hashes) for each material event.

Harvest wisely. Realize losses to offset gains within the same fiscal year where permitted, but watch for local wash‑sale and anti‑abuse rules that can disallow quick repurchases or related‑party round‑trips. For larger portfolios, place trading or treasury activity in vehicles with real substance-mind-and-management onshore, local directors, banking, office, and records-so outcomes align with facts, not form. Coordinate distributions, withholding, and CFC/management‑and‑control rules so your structure survives scrutiny and your cash actually flows where intended.

- Loss playbook: quarterly P&L checks; harvest into materially different assets; document purpose and price sources.

- Holding periods: preserve long‑term clocks where they matter; avoid resetting inadvertently via wraps or migrations.

- Execution: use DEX aggregators to minimize slippage; track gas as basis; record MEV impacts on proceeds.

- Entity kit: local board meetings, payroll or contractors, lease, bookkeeping, and tax filings; contemporaneous transfer‑pricing support.

- Distribution design: plan dividends vs. salary; check treaty relief and foreign tax credits before year‑end.

| Jurisdiction | Residency trigger | Basis method | Loss offsets | Substance focus |

|---|---|---|---|---|

| Germany | Domicile/183 days | FIFO or Specific ID | Private-sale losses offset private-sale gains | Management & control location |

| Portugal | 183 days/home | FIFO common | Within same category | Local presence for business income |

| UAE | 183 days/TRC | Consistent method | Personal CG often N/A | Economic Substance Regulations |

| Singapore | 183 days | Specific ID accepted | Trading losses only | Mind & management onshore |

Future Outlook

As 2025 unfolds, the landscape of crypto taxation looks less like a single rulebook and more like an atlas. The outlines are familiar-classification, sourcing, reporting, and rates-but every jurisdiction sketches them in its own hand. Common threads are emerging: tighter transparency regimes, clearer treatment of staking and DeFi, and more precise rules around NFTs and cross‑border flows. Yet the details still depend on where you stand, and sometimes on how long you’ve held, how you’ve used, and how you’ve reported.

Consider this guide a snapshot in motion. Laws evolve, thresholds shift, definitions harden, and new reporting frameworks come online. If your activity spans borders-or protocols-small differences in residency, timing, or record‑keeping can have outsized effects. Keeping clean books, tracking cost basis, and monitoring official updates will do more to reduce risk than any single tax strategy.

We’ve mapped the current contours country by country so you can navigate with confidence, not conjecture. Still, treat this as a compass, not coordinates. Before acting, verify with primary sources or a qualified advisor in your jurisdiction. The next legislative tide may not rewrite the map-but it can redraw the shoreline.