When the Federal Reserve trims rates by a quarter-point and markets barely blink, it’s tempting to call it a sell-the-news shrug. But beneath the calm tape, the story is more interesting. This week’s FOMC move-widely anticipated and the first cut since December 2024-came paired with a shift in the Fed’s own projections that could set the tone for the rest of the year.

In this post, we break down the key takeaways from the meeting and Jerome Powell’s Q&A, with a special focus on the dot plots and the Summary of Economic Projections. We’ll explore why the lack of immediate market reaction doesn’t tell the whole tale, how the Fed’s updated path points to the possibility of two additional cuts in October and December, and what a subtly dovish pivot could mean across asset classes. If you’ve been waiting for a clean signal, it may not be a headline-it may be in the fine print.

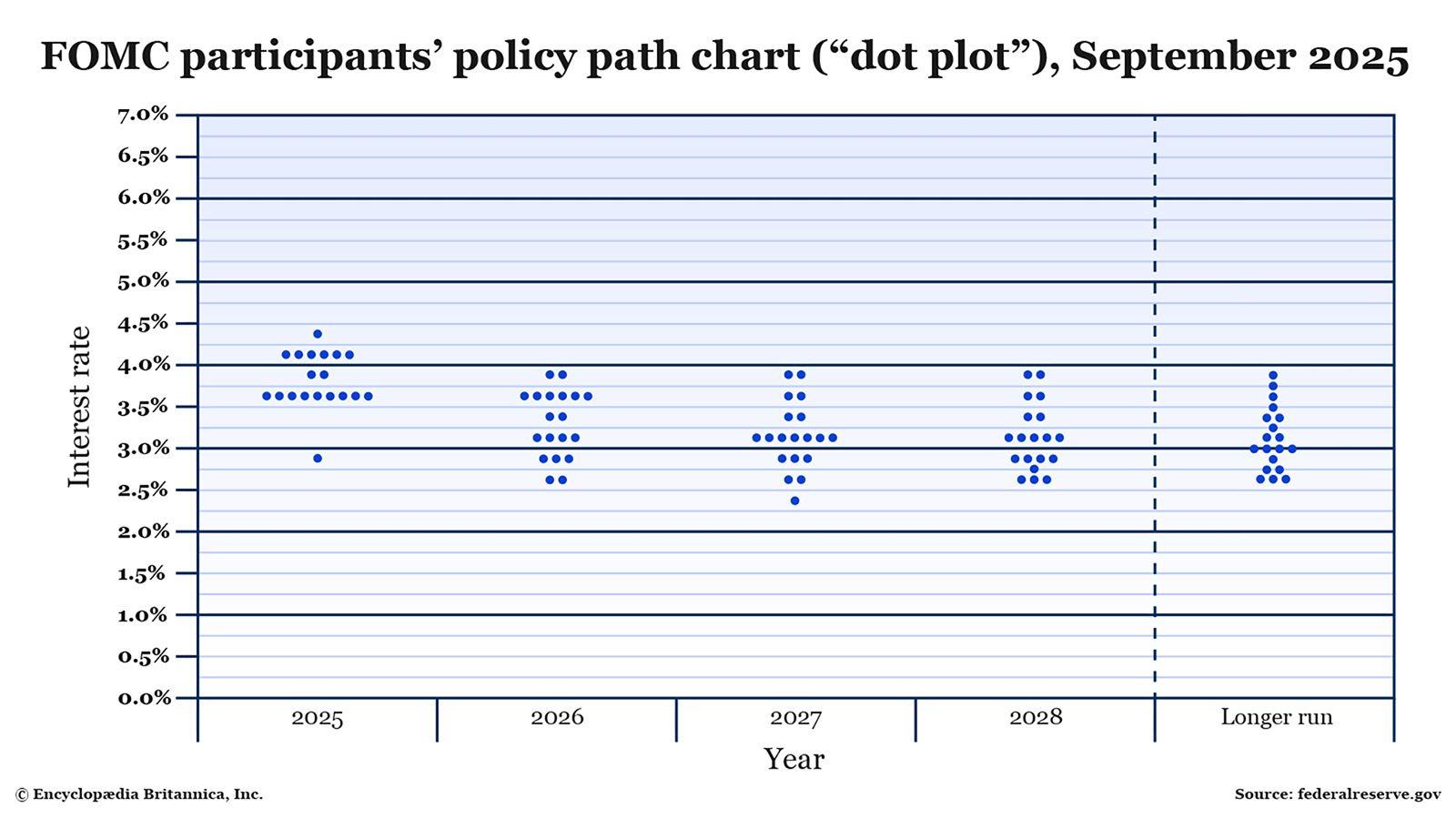

Dot plot reveals a dovish pivot pointing to two additional cuts by year end

Today’s 25 bps trim was the least interesting part-the surprise lay in the quarterly SEP and its dot plot, which shifted lower for the end‑of‑year target. That collective nudge signals an easing bias rather than a one‑off move, aligning with guidance that favors two incremental reductions across the next two meetings in October and December. Market reaction stayed muted because a cut was already ~95-98% priced going in; the new information is the trajectory, not the starting gun. Powell’s Q&A didn’t push back on that interpretation, reinforcing the sense that policy is transitioning from “hold” to “gradual calibration.”

- Dot plot drift: End‑year rate projections pivoted lower, clustering around a slower, step‑down path.

- Not a “sell the news” moment: The cut was priced; the path wasn’t-and that’s what anchors risk assets.

- SEP framing: Easing bias contingent on inflation progress and labor‑market balance-not an all‑clear.

In short, the Fed traded surprise for credibility of the glidepath. The base case now favors one cut per meeting into year‑end, barring an upside shock in inflation or re‑acceleration in wages. Remember: the path is a function of data, not dates. That’s why markets are calm today-the distribution of outcomes narrowed, even as the center moved a notch lower.

| Meeting | Signal from Dot Plot | Implied Move | What Flips It |

|---|---|---|---|

| October | Follow‑through on easing | -25 bps | Hot CPI / strong payrolls |

| December | Year‑end calibration | -25 bps | Core PCE re‑acceleration |

Priced in cut versus new guidance why the SEP matters more than the muted reaction

The 25 bps move was already embedded in pricing-roughly 95-98% odds going into the meeting-so a muted tape was inevitable. That doesn’t diminish the signal; it reframes it. The quarterly Summary of Economic Projections (SEP)-especially the dot plot-shifted meaningfully for the year-end federal funds target, which is the real story. Powell’s Q&A kept steering back to guidance, not the cut, and that guidance reads as a dovish-bullish pivot rather than a one-off “sell the news” moment.

- Base case priced: single 25 bps cut ≈ universally expected

- Surprise scenarios: double cut (~5%) or no cut (~0%) didn’t materialize

- Result: price action calm, but the path ahead recalibrated

| Focus | Pre-FOMC | SEP Signal |

|---|---|---|

| Today’s move | Single cut priced | No surprise |

| Year-end path | Unclear pace | More cuts implied |

| Market reaction | Muted | Guidance-driven repricing |

Why it matters now: the SEP reframes the next two meetings-October and December-as live for additional easing, not a singular cut to nowhere. The dot plot’s shift in the targeted end‑of‑year rate sets a timeline and a destination that traders can anchor to, turning a fully priced headline into a catalyst via forward guidance. In other words, the lack of fireworks today is the setup; the projected path is the spark.

- Quarterly cadence: the SEP updates the roadmap, not just the mile marker

- Policy bias: guidance tilts dovish, consistent with at least two more cuts

- Positioning cue: follow the dots, not the day-one reaction

October and December roadmap key data to monitor CPI core PCE labor slack and how each can shift probabilities

With the first 25 bp cut in the books and a notably more dovish set of dot plots, the path into the next two meetings hinges on how incoming inflation and employment data line up with the Fed’s Summary of Economic Projections. The near-term playbook is simple: if price pressures cool and labor slack builds, odds consolidate around back-to-back easings; if inflation proves sticky or labor tightens, the glidepath compresses to a single move or a pause. The market already priced the initial cut; what moves probabilities now is the sequence and tone of monthly prints rather than one-off surprises.

| Indicator | Dovish signal | Hawkish signal | Odds impact | Meeting tilt |

|---|---|---|---|---|

| CPI | Core cools, services ease | Core re-accelerates | Cuts odds ↑ | Brings Oct into play |

| Core PCE | Trend glides toward target | Sticky month-over-month | Steadies or ↓ | Shifts cuts to Dec |

| Labor slack | Unemp. edges up, openings fade | Wages firm, hiring broadens | Cuts odds ↑/↓ | Front-load vs. wait |

What to watch between now and year-end is less the headline and more the composition that Powell emphasized around the SEP: breadth of disinflation, durability of core trend, and whether the jobs market is easing without breaking. Tie each release back to the Fed’s updated projections and the Q&A tone: a cooler sequence in CPI and the Fed’s preferred core PCE validates the dovish pivot in the dots and lifts the probability of a follow-up in October, while any “sticky” streak postpones conviction to December as officials seek confirmation across multiple prints. Meanwhile, rising labor slack (higher unemployment, softer wage growth, fewer job openings) reduces the risk of overtightening and nudges the committee toward delivering the second move sooner rather than later.

- CPI: Prioritize core services; fading shelter impulse and softer medical/transport can tip odds toward an earlier cut.

- Core PCE: Month-over-month momentum is the tiebreaker; clean disinflation across goods and services aligns with the SEP’s dovish tilt.

- Labor slack: A gentle rise in unemployment with cooler wages supports easing; a re-tightening pushes decisions to December or beyond.

- Dot plots/SEP: The latest projections anchor the year-end target lower; subsequent data either validate two steps or trim the path to one.

Strategy shifts for easing extend duration modestly favor high quality rate sensitive equities and keep dry powder for post meeting volatility

The quarter-point cut was widely priced, but the dot plots and Q&A signaled a dovish follow‑through into the October and December meetings-making this less a “sell the news” blip and more a trend to position around. That backdrop argues to modestly extend duration rather than sprint to the long end: lean into high‑quality sovereigns and IG credit where carry can compound if the policy path softens from here, while keeping convexity risk controlled. With immediate market impact muted, the edge comes from thoughtful sizing and laddering rather than bold timing.

- Duration tilt: Add incrementally across the belly; avoid overloading the 30‑year until the path of cuts firms.

- Quality filter: Prioritize balance‑sheet strength and predictable cash flows over high beta.

- Entry discipline: Stagger buys around data drops and press conferences; let spreads/volatility do the inviting.

Lower projected policy rates into year‑end tend to modestly favor high‑quality, rate‑sensitive equities-think durable dividends and clear pricing power-while maintaining dry powder for the inevitable post‑meeting chop. This isn’t a license to chase; it’s a green light to upgrade quality, harvest carry, and be ready to buy weakness if the next SEP or presser shakes positioning without altering the dovish trajectory.

| Tilt | Why Now | Risk Check | Horizon |

|---|---|---|---|

| Duration + (belly) | Dovish dot plots; carry | Curve steepener risk | 1-3 months |

| Quality rate‑sensitives | Lower discount rates | Earnings revisions | Quarter‑end |

| Dry powder | Post‑meeting swings | Opportunity cost | Event‑driven |

In Conclusion

If today’s 25 bps cut felt like a ripple, the dot plot is the current beneath it. The headline move was priced; the story is the path. Powell’s Q&A and the SEP point to a gentler glide path for policy, with the Fed’s own projections tilting toward at least two more trims by year-end. That’s why this isn’t a one-and-done “sell the news” moment-it’s a recalibration of the destination.

From here, the compass points are clear: incoming inflation prints, labor-market cooling, financial conditions, and any shifts in the October and December meetings. We’ll keep tracking how futures, the dots, and the language evolve-because the market’s quiet today can still foreshadow a different tone tomorrow.

Thanks for reading. If you see a different signal in the dots, or think the market has it wrong, share your take-this story is written one meeting at a time.