There is no single “crypto price.” At any moment, bitcoin, ether, and countless tokens wear slightly different stickers depending on which exchange you ask, which currency you use, and how fast the rails beneath them are moving. Arbitrage lives in those gaps-small differences that appear at the edges between markets.

For beginners, crypto arbitrage is less about chasing windfalls and more about learning to measure the narrow space between spread and friction. It asks practical questions: Is the price difference larger than the fees, slippage, and transfer delays? Will withdrawal limits, network confirmations, or funding rates erase the advantage before you can capture it? In a market that runs nonstop and spans spot, futures, and perpetual swaps across dozens of venues, edges can form for many reasons-fragmented liquidity, fiat on-ramps, stablecoin flows, or sudden volatility-then vanish just as quickly.

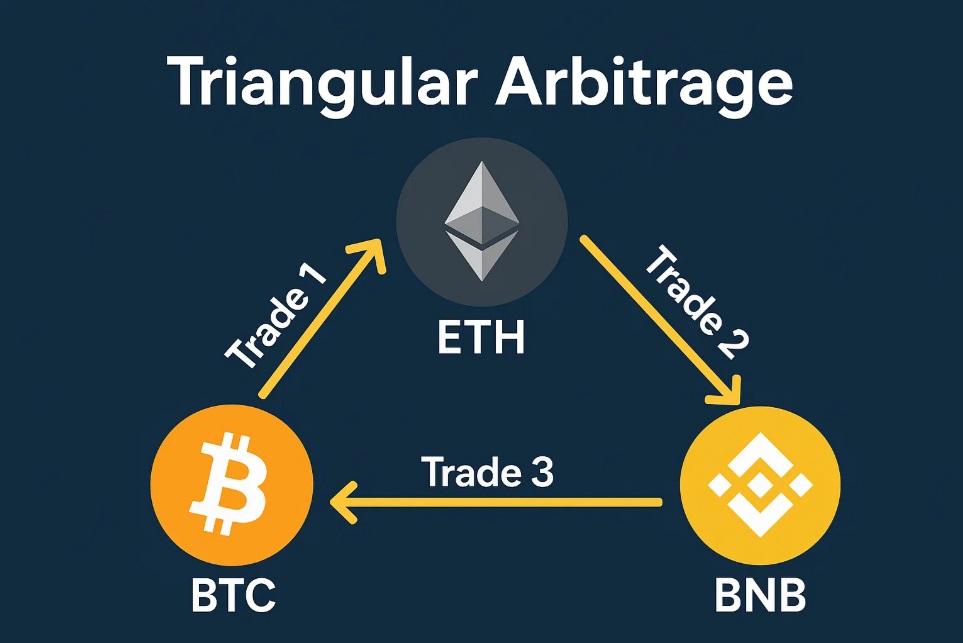

This article maps the terrain. You’ll see what arbitrage is (and isn’t), where price gaps typically emerge, and how basic strategies-cross-exchange, triangular, and funding-rate plays-actually work. You’ll learn to build a simple checklist for feasibility, track costs that matter, and understand operational risks like latency, custody, compliance, and tax considerations. No hype-just the mechanics, the math, and the mindset required to look for edges, evaluate them, and cross only when the path is clear.

Where edges emerge market structure spreads and liquidity pockets

Price dislocations tend to appear where microstructure is stressed: during regime shifts, at round-number magnets, around prior highs/lows, and when makers pull quotes. As volatility spikes, spreads widen, order books thin, and quotes go stale across venues-creating temporary gaps between a fast venue and a slower one. On derivatives, funding flips and basis kinks can decouple perp prices from spot, while on-chain congestion or stablecoin frictions can skew DEX pricing. These are the moments when inventory constraints, latency, and fragmented liquidity briefly outweigh theoretical efficiency, leaving room for disciplined arbitrage.

Convert those blips into repeatable trades by tracking effective spread after fees, slippage at your size, and the depth around your entry/exit. Focus on areas where liquidity clusters-session opens, listings, unlocks, and funding timestamps-then pre-map routes for the fastest leg. Keep a small, adaptive playbook that prioritizes execution quality and caps exposure time, because the edge lives in milliseconds to minutes, not hours.

- Cross-venue gap: Quote delta > total fees + buffer

- Funding skew: Perp premium/discount vs spot exceeds carry

- Stablecoin drift: Minor depegs create FX-like spreads

- Illiquid tails: Wide quotes and thin depth around round numbers

- Event windows: Listings, rebalances, and network congestion

| Edge | Signal | Action | Risk |

|---|---|---|---|

| Spot vs Perp | Perp > Spot + fees | Short perp, buy spot | Funding flip |

| CEX vs DEX | DEX lag, thin book | Buy DEX, sell CEX | Gas/spread shock |

| Stablecoin FX | USDT ≠ 1.000 | Arb via quote base | Redeem latency |

| Regional Split | Asia/EU price gap | Route to rich venue | Transfer delays |

Building your toolbox data feeds screening rules and alert workflows

Start with market data you can trust: aggregate multiple exchange APIs (REST for reference, WebSocket for speed), normalize symbols, and stamp everything with a single clock. Track L2 order books, funding rates, borrow costs, and fee schedules, then merge them into a clean view of executable spread after taker fees, expected slippage, and transfer costs. Build resilience: retries, circuit breakers, and venue health probes reduce false positives. For a beginner-friendly stack, pair a simple cache with a lightweight message bus so your screeners read the same, consistent snapshot.

- Spot + Perps feeds for cross-market basis clues

- L2 depth to gauge real fillable size, not just quotes

- Funding/borrow to price carry into net PnL

- Fees/limits (taker, withdrawal, rate limits) to avoid phantom edges

- Status pings for API latency, dropped channels, and throttling

| Rule | Purpose | Trigger | Action |

|---|---|---|---|

| Spread z-score | Spot outliers | z > 3, size ≥ $5k | Alert: “Alpha:Spread” |

| Depth gate | Ensure fill | Top-5 bids ≥ 2x order | Mark “Fill-OK” |

| All-in PnL | Net viability | After fees > 0.25% | Queue trade |

| Transfer check | Time + cost | ETA < 3m, fee < 0.05% | Allow move |

| Venue health | Mute noise | Heartbeat > 10s | Snooze venue |

Turn signals into decisions: channel alerts where you live (Telegram, Slack, webhooks), add cool-downs to reduce alert storms, and require multi-condition confirmations (spread + depth + fees) before escalation. Use severity tiers: info for watchlist, warning for investigate, critical for “arm execution.” Bake in risk gates-KYC region blocks, blacklist checks, max venue exposure-and attach a plain-English runbook link to each alert so you know the next step instantly. Keep logs of every signal and response to refine your thresholds with quick backtests.

- Tools: CCXT/ccxws for data, InfluxDB/Timescale for ticks, TradingView/Webhooks for triggers

- Filters: hysteresis bands, spread decay timers, liquidity floors per venue

- Escalation: notify → confirm → simulate → execute → verify

- Observability: dashboards for z-score, fill ratio, latency, mute list, and error rates

- Review loop: weekly threshold tuning from realized PnL vs. model

Executing the trade routing orders managing transfers and timing windows

Route legs like a chess puzzle: treat each venue as a square with its own latency and fee. Split the parent order into child orders with IOC/FOK constraints, cap per-venue exposure, and set a strict slippage budget. Pre-fund hot wallets where latency is unpredictable, and dry-run with tiny probes to confirm live deposit credit times. Bake network conditions into your quotes (gas spikes, mempool backlog), and lock routes that pass your thresholds while queuing alternates in case liquidity shifts mid-flight.

- Pre-flight checks: wallet allowlist status, min deposit/withdrawal, maintenance flags, per-asset transfer caps

- Latency map: venue order ack times, chain confirmations, exchange credit schedules

- Cost model: taker fees, maker rebates, L2 gas/priority tips, hidden spreads

- Controls: max age for quotes, cancel-on-fail, hedge venue in reserve, kill-switch

| Network | Confs | Deposit credit | Fee level | Use case |

|---|---|---|---|---|

| BTC | 2-3 | 20-60 min | High/Variable | Pre-fund, hedge elsewhere |

| ETH | 20-40 blocks | 2-5 min | Moderate | Fast spot/perp hops |

| Solana | Finality | 10-30 sec | Low | Rapid cycling |

| TRON | 20+ | 1-2 min | Low | Stablecoin shuttles |

Time the windows, not the candles: execute the fastest leg first if it locks the edge, or the slowest leg first if inventory risk dominates. Use staggered triggers: on-venue fills fire webhooks to initiate transfers, while a watchdog re-prices legs every few seconds with live gas and order book depth. Treat T+Δ (exchange credit delay) as inventory time; apply haircuts to edges that won’t survive the window, and prefer internal netting or perps hedges when transfer risk rises.

- Execution hints: auto-cancel if basis drifts > X bps, re-route to pre-funded venue

- Hedging: lock synthetic exposure on perps; unwind when funds land

- Batching: group small transfers; avoid peak congestion hours where possible

- Health checks: if credits exceed SLA, freeze new legs and raise edge threshold

Risk controls that stick fee modeling slippage buffers and capital allocation

Price edges vanish if you misprice costs, so treat every leg as a ledger entry: maker/taker fees per side, funding/borrowing, withdrawal/network tolls, and balance transfer frictions. Convert all costs to the same unit (bps or %) and subtract them from the gross spread to get a pre-trade net. Then layer in a slippage estimate from live order book depth and historical fill data, plus a conservative safety buffer to cover latency, partial fills, and queue position decay. Calibrate buffers by venue and time-of-day, and only greenlight routes where the net edge still clears your minimum threshold after these deductions.

- Model fees fully: maker/taker per side, FX, funding, borrow, gas/withdrawal, conversion.

- Stress slippage: use worst-of recent fills, add latency and partial-fill penalties.

- Hard guards: cancel-if-not-filled timers, max price impact per leg, stale-quote detection.

- Dynamic buffer: widen during volatility spikes; shrink after sustained clean fills.

| Route | Gross | Fees | Slippage | Buffer | Net | Action |

|---|---|---|---|---|---|---|

| Spot A↔B | 0.60% | 0.20% | 0.15% | 0.10% | 0.15% | Go |

| Perp-Spot | 0.45% | 0.18% | 0.12% | 0.10% | 0.05% | No-Go |

| Triangular A/B/C | 0.90% | 0.30% | 0.25% | 0.15% | 0.20% | Go |

Capital should flow to the cleanest fills, not just the fattest spreads. Use venue-level limits, route caps, and a volatility-scaled sizing rule (e.g., fraction of Kelly or fixed risk-per-trade) to prevent concentration. Impose open-leg exposure caps and drawdown throttles that automatically shrink size after slippage spikes or multiple partials. Maintain inventory bands and rebalancing budgets to avoid paying hidden costs to shuttle funds. Finally, wire a global kill switch that halts routing when realized costs breach modeled buffers.

- Size by risk: risk-per-trade ≤ X bps of equity; tighter during high volatility.

- Cap exposure: per exchange, per asset, per route; limit concurrent legs.

- Adaptive throttle: reduce size after N adverse fills; restore after clean streaks.

- Inventory bands: pre-set min/max balances; rebalance only when edge > transfer costs.

In Conclusion

Arbitrage lives in the seams-the thin lines where prices, venues, and moments don’t quite match. For beginners, the “edge” isn’t a secret signal so much as a routine: clean data, fee-aware math, disciplined execution, and a habit of measuring what actually happened. Whether you look across exchanges, within a single order book, or over different chains, the core remains the same: small, repeatable bets that respect frictions, not grand predictions.

Edges are also perishable. Latency, liquidity, fees, withdrawal limits, custody risks, and changing rules can turn a tidy spread into noise. Start by practicing with paper trades, time your pipeline end to end, record every assumption, and stress-test your worst cases before you scale. Keep an eye on compliance and tax obligations in your jurisdiction; the spread you ignore there is often the one that matters most.

In the end, finding edges is more craft than chase. Markets will blur and sharpen; your process should stay steady. If you can be as patient with your logs as you are quick with your fills, the map gets clearer. Walk the seam carefully, and let consistency-not excitement-do the heavy lifting.