Money is a promise-kept by different systems in different ways. On one side sits traditional currency: government-issued, centrally managed, and woven into the legal and banking infrastructure most of us use every day. On the other side are stablecoins: digital tokens designed to mirror the value of assets like the U.S. dollar, but moving across blockchains with software-based rules.

The comparison matters because both models aim to deliver the same core service-reliable value and usable payments-while making very different trade-offs. Stablecoins promise programmability, near‑instant settlement, and global reach, but rely on reserve management, technical security, and evolving regulation. Traditional currencies offer legal tender status, central bank stewardship, and established consumer protections, but can be slower, costlier across borders, and less flexible for automated finance.

This article lays out a clear, side-by-side view of how stablecoins and traditional currency differ across key dimensions: value stability and backing, trust and governance, speed and cost, access and inclusivity, privacy and transparency, regulation and consumer protection, monetary policy implications, and systemic risk. The aim is not to crown a winner, but to help you understand what each does well, where each falls short, and which use cases suit them best-whether you’re a curious consumer, a business weighing payment options, or a policymaker shaping the rules of tomorrow’s money.

Under the hood of stability: peg mechanisms versus monetary policy, practical risk checks for users

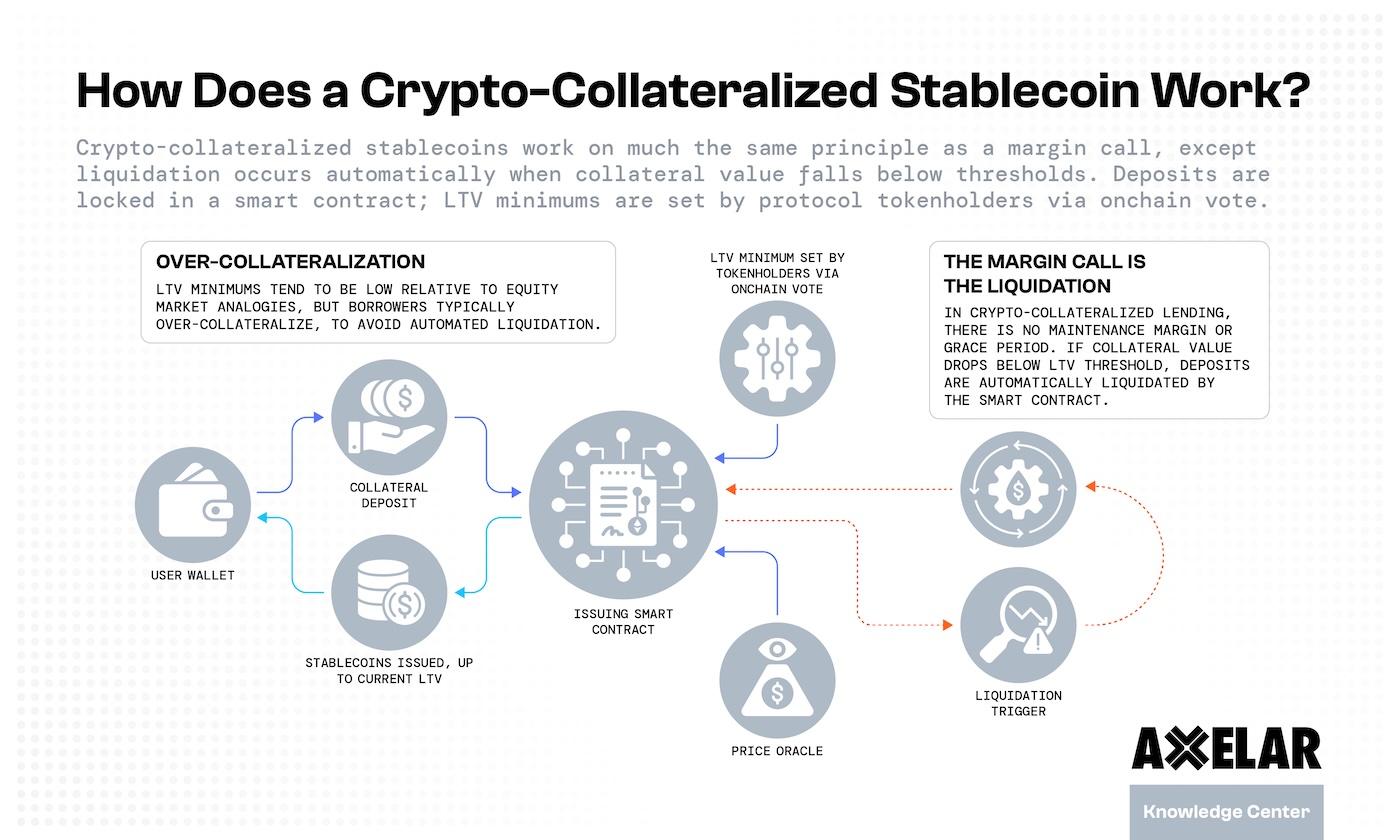

Price stability is engineered very differently across digital tokens and national money. Asset-backed stablecoins promise 1:1 redemption against reserves, crypto-collateralized versions rely on overcollateralization and liquidations, and algorithmic designs modulate supply or use market-maker incentives. By contrast, fiat currencies lean on human-led levers-interest rate policy, open market operations, and lender-of-last-resort facilities-to smooth cycles and absorb shocks. The trade-off is clear: code can be fast, transparent, and rule-bound but may be brittle under extreme stress; policy is elastic and shock-absorbing but arrives with lag, discretion, and political constraints.

- Stablecoin pegs: fiat-backed custody, crypto-backed vaults, or algorithmic supply rules.

- Policy toolkit: rates, reserves, asset purchases/sales, liquidity windows.

- Backstops: redemptions and arbitrage versus central bank balance sheet support.

| Track | Stablecoins | Traditional Currency |

|---|---|---|

| Anchor | Hard peg to asset | Inflation target |

| Stabilizer | Arb + collateral | Rates + OMOs |

| Backstop | Reserves/redemption | Central bank |

| Transparency | On-chain + attest | Reports/minutes |

| Stress signal | Depeg, low depth | FX slide, CPI spike |

Before holding, saving, or settling with any unit, run quick, practical checks focused on redeemability, liquidity, and governance. Read short-form attestations and audit names, test small redemptions, and scan market depth where you actually trade. Map what can go wrong-custody freezes, smart contract bugs, oracle failures, or policy shifts-and decide how much discretion versus code you’re comfortable with. Diversify across issuers and mechanisms if you need uninterrupted parity.

- Reserves: attestations frequency, custodian list, asset mix, concentration.

- Redemption: fees, windows, KYC/limits, historical fulfillment rate.

- On-chain risk: audit reports, upgrade keys, pause/blacklist powers.

- Market depth: order books, AMM TVL, slippage at your ticket size.

- Track record: past depegs, recovery time, incident transparency.

- Jurisdiction: regulator posture, enforcement history, sanctions exposure.

- Custody: self-custody readiness, multisig, withdrawal rehearsal.

- Mix: hold a blend (fiat-backed + overcollateralized) to reduce single-point failure.

Liquidity, settlement speed, and fees by use case: retail payments, remittances, and treasury operations

Retail payments thrive on immediacy: stablecoins offer settlement speed in seconds with network-level fees that can be pennies, while card rails batch behind the scenes, clearing next day and charging blended merchant fees. On the liquidity side, digital wallets and exchanges provide 24/7 access, enabling quick conversions to local currency; in contrast, cash management for card and bank payments typically follows business hours and cutoffs. For merchants, the trade-off is between ultra-fast finality and the need for reliable on/off-ramps and point-of-sale integrations. In short, stablecoins compress fees and latency, but traditional processors still win on ubiquity and built-in consumer protections.

| Use case | Stablecoins | Traditional rails |

|---|---|---|

| Retail | Seconds; low fees; 24/7 liquidity | T+1-T+2; 1.5-3%+; bank hours |

| Remittance | Minutes; <1% typical; ramp-dependent | 1-5 days; 3-7%+FX; cash networks |

| Treasury | Near-instant; basis-point costs; programmable | Same-day wire/ACH; fixed fees; batch windows |

Remittances benefit dramatically when value crosses borders without correspondent chains: stablecoins reduce hops, shrink FX spreads via crypto-liquidity pools, and deliver funds to mobile wallets quickly-though the last mile still hinges on local exchanges and compliance. For treasury operations, programmable settlement and always-on liquidity make internal transfers, sweep strategies, and cross-entity netting faster and cheaper than wires, yet many enterprises keep a dual stack: stablecoins for intraday mobility and traditional rails for payroll, payables, and audited cash forecasts. The choice often boils down to operational risk tolerance, auditability, and the cost of on/off-ramp friction versus the predictability of legacy rails.

- Speed-first workflows: stablecoins shine where minutes matter and batch windows hurt.

- Fee sensitivity: micro-margins favor low network costs over percentage-based interchange.

- Liquidity access: global, 24/7 depth helps-unless local ramps are thin or regulated tightly.

- Control vs. coverage: programmability and finality vs. universal acceptance and chargeback norms.

Compliance, transparency, and counterparty risk: a due diligence checklist before adopting stablecoins or bank alternatives

Before replacing cash balances with tokenized dollars or non-bank rails, frame the review like a treasury-grade vendor assessment. Validate who regulates the provider, what rights you have over funds, and how quickly you can exit in stress. Seek primary-source evidence-licenses, audited financials, legal opinions, reserve attestations-and confirm jurisdictional exposure and insolvency outcomes. Align onboarding and monitoring with your own compliance program so that sanctions, reporting, and data handling don’t become hidden liabilities.

- Regulatory standing: Active licenses/registrations (e.g., MSB, e‑money, MiCA) and named supervisors; enforcement history disclosed.

- Reserve transparency: Independent attestations or audits, daily balance snapshots, asset mix (cash/T‑bills/repos), segregation and custodians.

- Redemption mechanics: 1:1 terms, cut‑off times, fees/minimums, counterparties used, settlement rails, pause/blacklist policies.

- Legal structure: Bankruptcy remoteness, trust/nominee arrangements, customer claim priority, governing law, dispute resolution.

- KYC/AML & sanctions: Travel Rule readiness, screening vendors, ongoing monitoring cadence, reporting SLAs, geographic blocks.

- Technology risk: Smart‑contract audits, key management, change controls, chain exposure, uptime/SLA, incident history.

- Data & privacy: GDPR/CCPA alignment, data residency, retention, API logging, third‑party sharing.

- Insurance & safeguards: Scope and limits (noting that most tokens are not FDIC/SIPC insured), fidelity/cyber coverage.

- Governance: Board and committees, disclosures cadence, treasury policy, conflicts management, key‑person risk.

Counterparty risk is more than credit: it blends liquidity, operational resilience, legal enforceability, and market structure. Score each vector (low/medium/high) and run exit drills: Can you redeem at par under stress, or reroute flows within 24-48 hours? For tokens, scrutinize collateral quality and concentration, de‑peg history, and admin controls; for bank alternatives, evaluate safeguarding arrangements and the legal status of client funds. Keep a living heatmap so procurement, legal, and treasury share one view of thresholds, waivers, and residual risk.

| Checkpoint | Stablecoin | Bank alternative | Red flag |

|---|---|---|---|

| Reserves/collateral | T‑bills, cash, segregated | Safeguarded e‑money/insured deposits | Commercial paper, opaque loans |

| Attestation/audit | Monthly attest; annual audit | External audit; prudential reports | No independent verification |

| Redemption | Direct 1:1 for KYC clients | Same‑day withdrawals/transfers | Pauses, gates, high minimums |

| Legal claim | Claim on reserve trust | Client funds safeguarded/insured | Unsecured, commingled funds |

| Ops & controls | Audited contracts, multisig, limits | Dual control, uptime SLA, DR | Single admin key, weak DR |

Portfolio strategy for organizations and individuals: when to hold stablecoins, when to prefer deposits or cash

Organizations can treat money rails as interchangeable tools: route operating flows through what clears fastest and safest, and park reserves where risk is lowest and reporting is cleanest. Use stable-value crypto for programmatic, cross‑border, 24/7 settlement and on‑chain commerce; default to insured deposits for payroll, taxes, and vendor invoices that require traditional rails; keep a thin layer of physical cash for blackout scenarios and bank‑outage resilience. Segment treasury into operating (0-30 days), buffer (1-3 months), and reserve (3-12 months) buckets so each can live on the most efficient rail for its job.

| Use case | Lean to | Key driver |

|---|---|---|

| Global supplier payout | Stablecoins | 24/7 finality, low FX spread |

| Payroll, taxes, rent | Insured deposits | Compliance, ACH/wires |

| Crisis continuity fund | Physical cash | Power/rail outages |

| Idle cash (1-4 weeks) | Deposits/MMF via bank | Yield, low op‑risk |

| On‑chain revenue | Stablecoins | Composability, speed |

- Tilt toward stablecoins when weekend or cross‑time‑zone settlement is critical; on‑chain receipts or payouts exceed a set threshold; programmatic disbursements matter; you want instant FX routing between USD/EUR/other stablecoins.

- Favor deposits when insured coverage is paramount; auditors require clear bank statements; counterparties prefer ACH/wire; your ERP and approval flows are bank‑native.

- Hold cash when you plan for disaster recovery, face regional banking stress, or need petty cash and immediate physical access.

For individuals, keep your safety net simple: maintain an emergency fund of 3-6 months in insured deposits and a small cash cushion, then use stable-value crypto for specific jobs-low‑cost remittances, instant transfers across borders, or interacting with on‑chain apps-while periodically converting back to bank rails for living expenses. Weigh smart‑contract risk and issuer risk against bank and policy risk; diversify issuers and chains if you actively use stablecoins, and redeem to your bank on a cadence that suits your budget cycle.

To Conclude

Set side by side, stablecoins and traditional currency look less like rivals and more like two instruments in the same orchestra-different timbres, shared tempo. One offers programmability, always-on settlement, and global reach; the other brings universal recognition, mature safeguards, and well-understood rules. The comparison isn’t about crowning a winner so much as clarifying when each plays lead and when each should keep time in the background.

Your choice will hinge on the job to be done. If immediacy, automation, and cross-border flow matter most, the digital rails of stablecoins may fit. If regulatory certainty, offline usability, and broad acceptance are paramount, traditional money remains the sturdier path. Each carries trade-offs: reserve transparency and counterparty risk on one side; intermediaries, hours, and friction on the other.

The road ahead likely belongs to coexistence and gradual convergence-tokenized deposits, improved payment rails, clearer standards, stronger audits, and, perhaps, public digital money. As the landscape evolves, treat money like infrastructure: define the requirements, test assumptions, and align the medium with the mission rather than the headlines.

In the end, stability isn’t a label-it’s a match between design, oversight, and use case. Choose the instrument that keeps your rhythm steady, and be ready to change tempo as the score of finance continues to be rewritten.